For most of the past decade, tech operated under a simple formula: grow fast, expand teams, capture market share, and optimize later.

That formula worked in a zero-rate world. It works less well in a disciplined capital environment.

What we’re seeing in 2025 and early 2026 isn’t tech collapsing. It’s tech maturing under tighter economic rules.

Demand for technology hasn’t disappeared. Cloud infrastructure is still expanding. Cybersecurity spending is still rising. AI investment is accelerating. But the economic framework around tech has shifted, and that changes behavior quickly.

Let’s look at what the data actually says.

1. Capital Is Still the Primary Driver

The biggest force shaping tech right now isn’t AI. It’s capital discipline.

As of early 2026, the Federal Reserve’s target rate remains elevated compared to the pre-2022 era, hovering in the mid-3% range following gradual reductions from peak tightening levels. The zero-rate environment that defined 2010–2021 is clearly over.

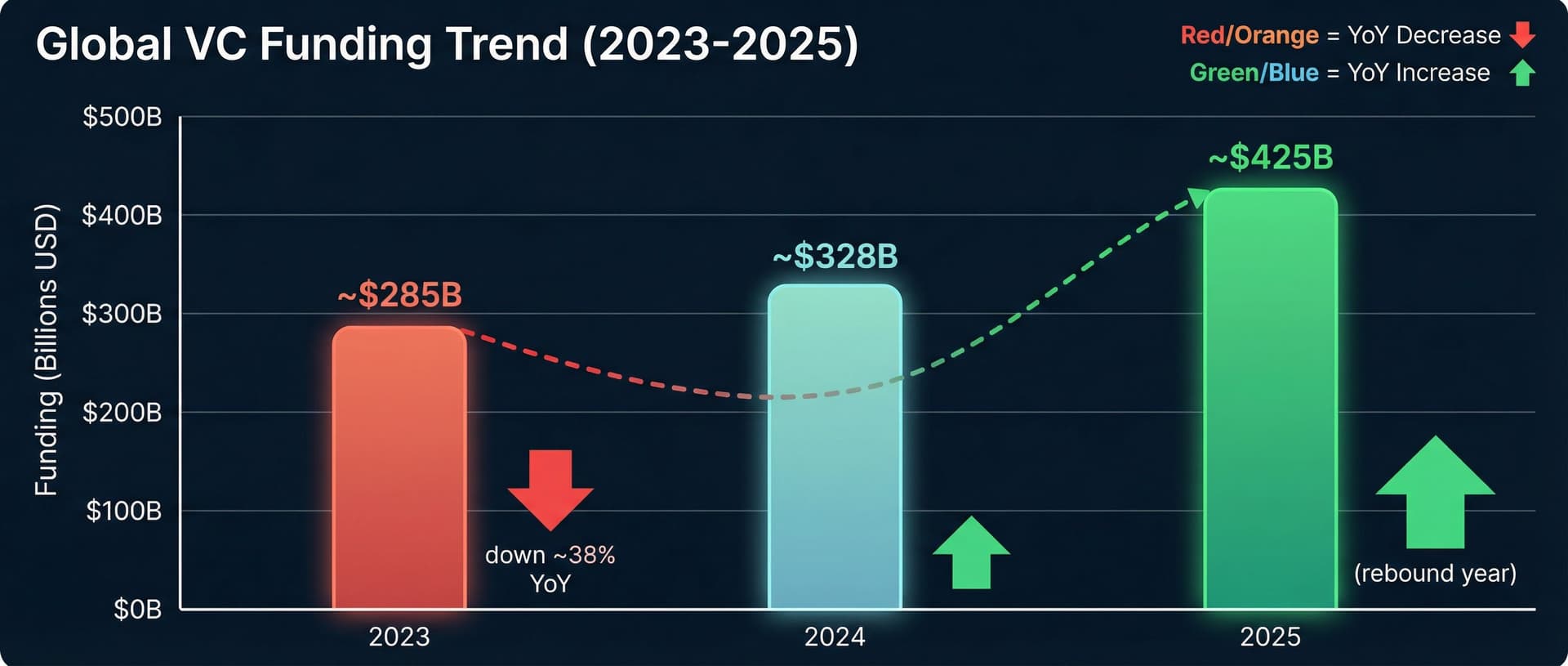

Venture Funding: Not Dead, Just Repriced

After the 2021 peak, global venture capital fell sharply:

That rebound is important.

Tech capital didn’t vanish. It rotated. Investors became selective, then returned to sectors showing productivity leverage — particularly AI infrastructure, security, and enterprise efficiency platforms.

Investor enthusiasm around AI funding has cooled compared with the breakneck pace of 2024–2025. After record levels of venture investment — global AI startup funding surpassed $200 billion in 2025, up roughly 75% from about $114 billion in 2024 — momentum began to ease in late 2025 as deal volume slowed and investors became more selective. Reports show early-stage AI funding declined approximately 30–40% year-over-year in recent quarters, even as total capital deployed remained historically elevated. Public markets reflected a similar recalibration, with AI-heavy equities pulling back and capital rotating toward companies demonstrating clearer near-term revenue and measurable productivity gains.

2. Layoffs: Restructuring, Not Sector Collapse

Layoffs remain one of the clearest signals people feel. According to Challenger, Gray & Christmas:

At the same time, Challenger notes that restructuring, cost control, and economic conditions are leading reasons cited for cuts — not demand disappearance.

3. Hiring Has Slowed — And That’s the Quiet Signal

Often the bigger story is not layoffs but hiring restraint.

Challenger’s 2025 data shows that companies are not aggressively expanding headcount.

They are prioritizing productivity per employee.

That’s a maturity shift.

4. Growth Has Normalized — It Hasn’t Disappeared

Public tech firms are still growing, but at moderated rates compared to the 2010s.

Large-cap tech revenue growth in 2025 generally sits in mid-single to low-double digits depending on segment (cloud, AI infrastructure, enterprise SaaS).

This reflects:

In mature markets, growth is harder to capture — and that increases pressure on margins and efficiency.

5. AI’s Role — Real, But Contextual

AI investment is rising significantly in 2025–2026.

Crunchbase notes AI as a dominant funding category in 2025’s rebound year. Meanwhile, enterprise AI adoption continues accelerating in automation, internal copilots, workflow compression, and infrastructure optimization.

But here’s the key:

In an efficiency-focused market, AI becomes attractive because it helps companies respond to maturity pressure.

6. The Labor Market Is Polarizing, Not Collapsing

Even amid restructuring, core technical roles remain durable.

According to the U.S. Bureau of Labor Statistics (May 2024 data, latest full dataset available) data and security roles are among faster-growing occupations.

The market isn’t shrinking uniformly. It’s reallocating.

7. What This Really Is: Operational Maturity

Here’s the cleanest way to frame 2025–2026:

Tech is transitioning from:

Growth subsidized by cheap capital to growth filtered by efficiency and leverage.

A Friendlier Bottom Line

If you zoom out, tech in 2026 looks less chaotic than it feels.

Capital is flowing again — but more carefully.

Hiring continues — but more selectively.

Investment remains strong — but more ROI-driven.

That’s not decline.

That’s an industry growing up.

References & Further Reading

About the Author

Related Articles

Picking the Right Location Isn't a Gut Decision Anymore. Here's How Data Is Driving Ours.

Finding a new location comes with multiple financial and market inputs. We simplified the inputs to normalize our decision.

What If Your Business Intelligence Could 6x Your Revenue in One Quarter?

Increasing profit while reducing cost is the goal of every successful business.

HBCUs and the Post-Affirmative Action Era: Opportunity, Responsibility, and the Future of Higher Education

Historically Black Colleges and Universities have long played a critical role in shaping Black professional leadership in the United States. Following the Supreme Court’s decision to end race-conscious admissions, the higher education landscape is beginning to shift. Early data suggests changes in Black enrollment at some selective universities, while applications to HBCUs continue to grow. This moment presents both opportunity and responsibility. As the demand for HBCU education rises, institutions may need to rethink admissions standards, academic strategy, and their role in preparing students for an AI-driven economy where traditional career paths are rapidly evolving.